Moody’s Investors Service placed Tapestry Inc.’s Baa2 rating on review for a possible downgrade on Thursday, after the company said it’s buying Capri, the parent of Michael Kors, for about $8.5 billion in a deal that will be mostly funded with debt.

The move “reflects governance considerations, including the significant increase in debt with the Capri

CPRI,

acquisition and Tapestry’s new leverage target, which will drive a sustained increase relative to the company’s typical under 1x net debt/EBITDA,” Moody’s said in a statement.

The deal will be funded with bonds, term loans and balance sheet cash.

The company said it has secured $8 billion in committed bridge financing from Bank of America and Morgan Stanley. That makes it the biggest high-grade M&A financing of the year to date, according to Bloomberg, ahead of the $5.75 billion bridge loan that Nasdaq Inc.

NDAQ,

secured to fund its acquisition of software company Adenza from private-equity firm Thoma Bravo in June.

For more, see: Nasdaq stock suffering biggest selloff in 10 years as the deal to buy Adenza includes more than $4 billion in stock

Tapestry

TPR,

said it’s determined to retain its investment-grade rating by suspending share buybacks.

For more, read: Coach parent Tapestry to acquire Michael Kors parent Capri in cash deal valued at $8.5 billion

“Tapestry’s acquisition of Capri will increase its scale and customer reach by adding three valuable brands to its global luxury portfolio, while applying Tapestry’s direct-to-consumer focus and technology platform to grow profitability at Michael Kors, Versace and Jimmy Choo,” Moody’s Vice President-Senior analyst Raya Sokolyanska said.

“At the same time, the company’s new financial policy will result in materially higher leverage than in the past, and the acquisition itself will temporarily raise leverage well above the company’s under 2.5x target.”

As the following chart from data-as-a-service company BondCliQ Media Services shows, Tapestry has three outstanding bond series totaling $1.2 billion of debt. The bonds are due to mature in 2025, 2027 and 2032.

Outstanding Tapestry Inc. debt by maturity year (Total $1.2 billion). Source: BondCliQ Media Services

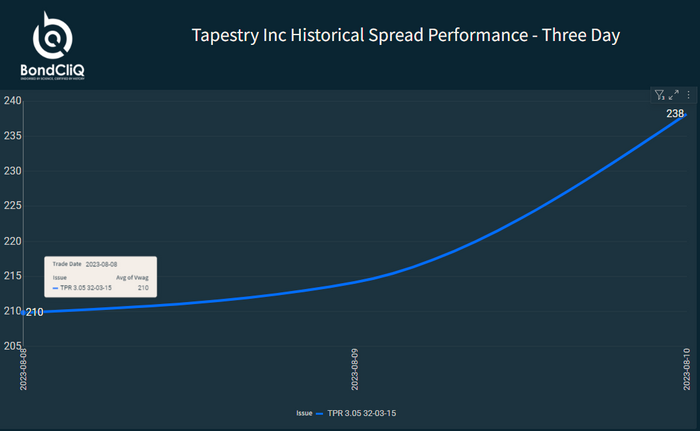

The next chart shows the performance of the most active bonds, the 3.05% notes that mature in March of 2032, over the last three days with spreads roughly 25 basis points wider. The news was broken late Wednesday by the Wall Street Journal.

Tapestry Inc. historical spread performance – three day. Source: BondCliQ Media Services

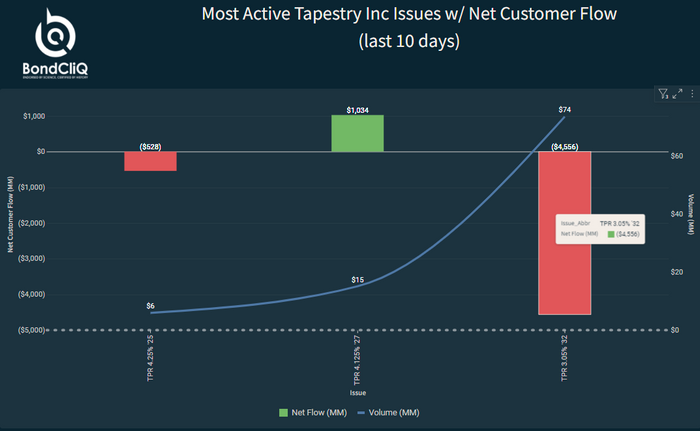

The next chart shows the last 10 days when there was net selling of the bonds.

Most active Tapestry Inc. issues with net customer flow (last 10 days). Source: BondCliQ Media Services

The stock was last down 16%.

Read the full article here